Defining the 2026 commodity landscape

The 2026 commodity supercycle is not a uniform surge; it is a structural divergence. We are witnessing a tension between persistent supply constraints and macroeconomic volatility. This environment redefines commodity trading in 2026, moving away from simple cyclical trends toward a fragmented market where technology and sustainability act as primary drivers.

Supply chains are tightening due to two converging forces. First, the global energy transition requires massive inputs of copper, lithium, and nickel, but new mine development lags behind demand. Second, geopolitical tensions and currency fluctuations are disrupting traditional trade routes. Investors now face a complex web of risks that extend beyond simple supply and demand curves.

The market is entering a more fragmented phase. Overall prices are projected to decline for a fourth consecutive year, driven by subdued global growth, yet specific sectors remain resilient due to structural deficits.

This fragmentation creates distinct opportunities. While broad commodity indices may show mixed signals, specific assets like gold and silver are hitting all-time highs amid global uncertainty. Precious metals are no longer just hedges; they are integral components of the tech-driven trade reshaping global markets.

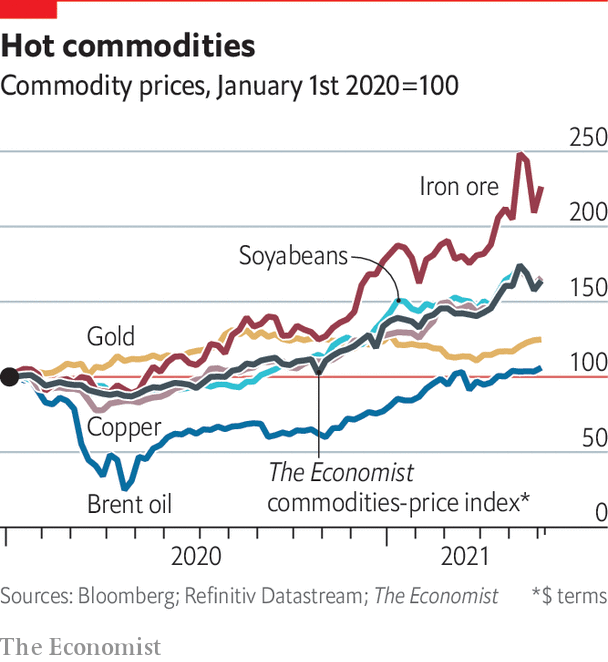

The following chart illustrates the recent performance of the Bloomberg Commodity Index, grounding this analysis in live market data.

AI reshaping supply chain efficiency

Artificial intelligence in supply chain management is shifting from experimental pilots to core production infrastructure. In 2026, this transition is defined by two concrete applications: logistics optimization and predictive maintenance for extraction assets. These tools are no longer theoretical; they are actively compressing margins and stabilizing output in volatile commodity markets.

Logistics optimization uses machine learning to manage the friction of global trade. Rather than relying on static routes, algorithms process real-time data on port congestion, weather patterns, and fuel costs to adjust shipping paths dynamically. This capability is critical when geopolitical tensions disrupt traditional corridors. By rerouting cargo before bottlenecks form, companies reduce idle time and lower the cost per ton of transported goods.

In mining and extraction, predictive maintenance has become the primary defense against unplanned downtime. Sensors on heavy machinery feed continuous data streams to AI models that detect micro-anomalies in vibration, temperature, and pressure. These models predict component failure weeks in advance, allowing operators to schedule repairs during planned windows. This approach prevents catastrophic breakdowns that can halt production lines for days, ensuring a more consistent flow of raw materials into the supply chain.

The integration of these technologies creates a feedback loop that strengthens market resilience. As AI systems learn from each operational cycle, their accuracy improves, further reducing waste and energy consumption. This efficiency gain is a key driver for the optimistic 2026 commodity outlook, as it allows producers to maintain profitability even as input costs fluctuate.

Geopolitics and the energy transition

Commodity markets in 2026 are caught in a structural vise. On one side, geopolitical fragmentation is disrupting established trade routes and supply chains, creating volatility that traditional hedging strategies struggle to contain. On the other, the global energy transition is driving unprecedented demand for critical minerals, forcing a reevaluation of resource security. This dual pressure is reshaping how nations and investors view commodities—not just as industrial inputs, but as strategic assets.

The shift toward green energy is particularly acute for copper and lithium. These metals are the backbone of electrification, from grid infrastructure to electric vehicles. However, supply constraints and mining delays mean that demand is outpacing production capacity. This imbalance is not temporary; it reflects a fundamental realignment of global industrial priorities. Nations are increasingly competing for access to these resources, leading to tighter markets and higher prices for downstream manufacturers.

Oil markets remain sensitive to geopolitical shocks, even as the long-term demand curve flattens. Recent tensions in key producing regions have kept prices elevated, adding to inflationary pressures. While the energy transition reduces oil's dominance over time, the immediate reality is a market still heavily influenced by political instability and supply disruptions. Investors must manage this complexity, balancing short-term volatility with long-term structural shifts.

Freeport-McMoRan (FCX) stock performance, reflecting copper market dynamics.

Comparing key commodity sectors

The 2026 commodity supercycle is not uniform; it is a fragmented landscape where AI-driven efficiency and geopolitical reshaping pull sectors in different directions. While broad indices may face headwinds, specific niches offer distinct risk-reward profiles for traders. Understanding the divergence between energy, industrial metals, and precious metals is essential for capital allocation.

Energy: The Efficiency Paradox

Energy markets are caught between sustained demand from AI data centers and the long-term pressure of electrification. Natural gas and power infrastructure are seeing renewed investment, while traditional oil faces structural substitution. The price outlook remains volatile, driven by OPEC+ discipline and shifting global trade routes.

Industrial Metals: The AI Infrastructure Play

Copper and aluminum are critical inputs for the grid upgrades required to support AI hardware. Supply constraints in major mining regions are tightening availability, creating a structural deficit that supports prices despite broader economic slowdowns. This sector is directly tied to the physical build-out of digital infrastructure.

Precious Metals: The Stability Anchor

Gold and silver continue to serve as hedges against currency debasement and geopolitical uncertainty. Recent all-time highs reflect a loss of confidence in traditional safe havens, positioning precious metals as a portfolio stabilizer. Unlike industrial metals, their value is driven less by utility and more by monetary policy expectations.

Sector Comparison

The table below contrasts the primary drivers for each sector to highlight where the 2026 supercycle offers the clearest opportunities.

| Sector | Supply Constraint | Demand Driver | 2026 Outlook |

|---|---|---|---|

| Energy | Moderate | AI Power & Grid | Volatile |

| Industrial Metals | High | Infrastructure Build | Bullish |

| Precious Metals | Stable | Monetary Hedge | Stable |

Investment outlook and risk factors

Commodities are poised for attractive returns in 2026, offering portfolio diversification amid supply-demand imbalances and geopolitical risks [1]. However, the high-stakes nature of this supercycle means volatility remains a constant companion. Currency fluctuations and shifting trade policies can quickly erode margins, turning potential gains into losses.

To manage this landscape, broad exposure is often safer than picking individual winners. While precious metals like gold have hit all-time highs [2], industrial metals tied to AI infrastructure and energy transition remain critical. Investors should consider a mix of commodity-linked equities and broad ETFs to balance sector-specific risks.

Diversification is not just about spreading assets; it is about hedging against the very forces driving the supercycle. As AI reshapes global trade, the ability to adapt to policy shifts will determine long-term success in commodity markets.

[1] https://www.ubs.com/us/en/wealth-management/insights/market-news/article.3002623.html [2] https://www.morganstanley.com/im/en-hk/intermediary-investor/insights/articles/trends-driving-optimism-in-2026.html

No comments yet. Be the first to share your thoughts!