2026 commodity trends

The 2026 commodity supercycle is no longer a theoretical projection; it is actively reshaping metal prices through AI-driven demand. As data centers and semiconductor manufacturing scale, the appetite for copper, aluminum, and rare earth elements has outpaced traditional industrial cycles. This structural shift means commodity trends in 2026 are defined less by macroeconomic cycles and more by the physical constraints of the digital economy.

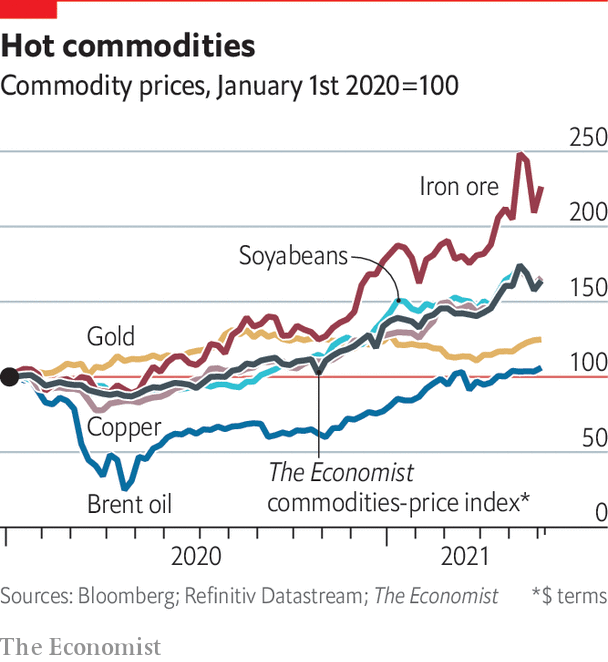

Base metal prices are expected to remain broadly stable or rise modestly, supported by a firm demand base that includes both green energy infrastructure and AI hardware production. While fuels and traditional industrial inputs face volatility from geopolitical tensions, precious metals like gold and silver are emerging as key sectors with a bright outlook. Investors are increasingly viewing these assets as hedges against the inflationary pressures inherent in supply-constrained metal markets.

The divergence between industrial and precious metals highlights a complex landscape. Industrial metals are tethered to the relentless growth of tech infrastructure, while precious metals benefit from monetary policy shifts and central bank buying. Understanding these distinct drivers is essential for navigating the market. The 2026 commodity trends suggest a bifurcated market where AI demand fuels industrial metals, while macroeconomic uncertainty supports precious metals.

2026 commodity trends choices that change the plan

The 2026 commodity supercycle is not a uniform surge. It is a fragmented market where AI-driven industrial demand collides with broader economic moderation. Morgan Stanley projects that base metal prices will remain stable or rise modestly, driven by the electrification of transport and data center infrastructure. However, the World Bank forecasts a general 7 percent decline in global commodity prices, marking the fourth year of post-pandemic moderation.

This divergence creates distinct tradeoffs for investors. You must decide whether to prioritize the high-growth, supply-constrained niches of the energy transition or the stability of broad-market inflation hedges. The following breakdown highlights the key sectors where these forces intersect, helping you evaluate which assets align with your risk tolerance and timeline.

| Sector | Primary Driver | Key Risk | 2026 Outlook |

|---|---|---|---|

| Copper | AI data centers & EVs | Supply bottlenecks | Strong structural deficit |

| Gold | Central bank buying | Strong USD rally | Resilient upside |

| Oil | OPEC+ cuts vs. demand | Recession slowdown | Volatile range-bound |

| Lithium | Battery storage growth | Overcapacity from 2023 | Bottoming & recovery |

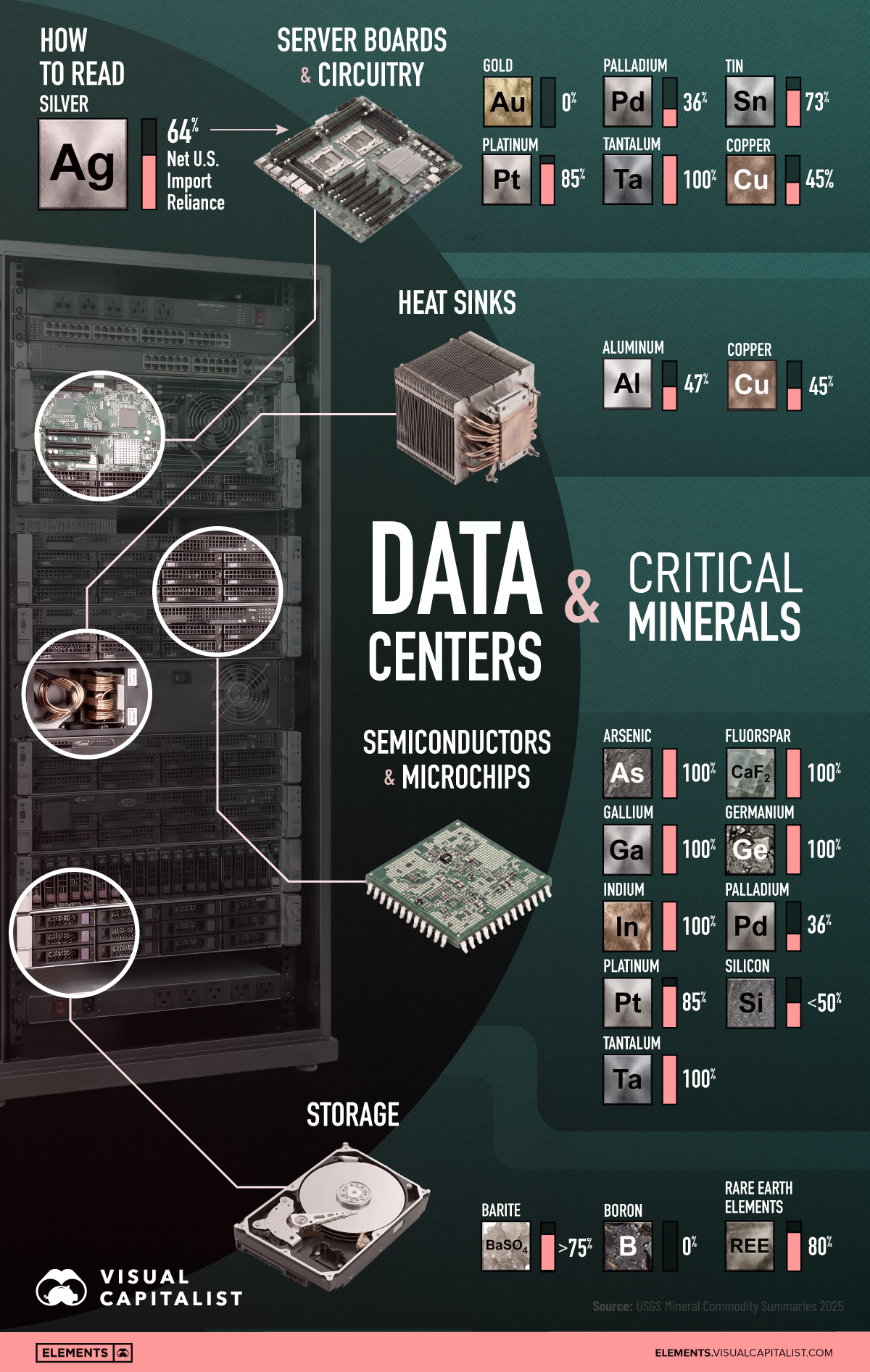

Copper: The AI Backbone

Copper is the most direct beneficiary of the AI hardware build-out. Data centers require significant electrical infrastructure, and electric vehicles use twice the copper of traditional cars. While supply is constrained by aging mines and permitting delays, demand remains inelastic. The tradeoff is price volatility; any sign of global manufacturing slowdown can trigger sharp corrections, even if the long-term trend is upward.

Gold: The Monetary Hedge

Gold’s 2026 outlook is supported by central bank accumulation and geopolitical uncertainty. Unlike industrial metals, gold does not rely on manufacturing growth. It acts as a portfolio stabilizer when real interest rates fall or when fiat currencies face debasement pressures. The risk lies in a sustained strong U.S. dollar, which typically weighs on non-yielding assets. However, structural buying from emerging market central banks provides a floor.

Oil: The Demand Dilemma

Oil markets face a classic tug-of-war between supply discipline and demand fragility. OPEC+ continues to manage supply to support prices, but non-OPEC production from the U.S. and Guyana is rising. Meanwhile, the transition to electric mobility and efficiency gains in emerging markets cap demand growth. The result is a volatile, range-bound market where geopolitical shocks cause spikes, but structural oversupply limits sustained rallies.

Lithium: The Recovery Play

Lithium prices have crashed from their 2022 peaks due to rapid supply expansion outpacing EV demand growth. However, 2026 marks a potential inflection point. As high-cost mines close and battery storage adoption accelerates, the market is expected to rebalance. This is a higher-risk, higher-reward play. Investors are betting on a bottoming process, but timing the recovery requires patience and tolerance for near-term volatility.

How to evaluate commodity exposure in 2026

AI infrastructure is no longer a speculative theme; it is a structural demand driver for specific metals. Copper, aluminum, and lithium are essential for data center power grids and battery storage, creating a persistent floor for prices. However, not all commodity sectors are moving in lockstep. Investors must distinguish between metals tied to energy transition hardware and those driven by macroeconomic hedging.

Use this framework to assess whether a commodity position aligns with current market realities.

Focus on metals with direct applications in data center construction and power distribution. Copper is the primary conductor, while aluminum reduces weight in transmission lines. Unlike broad industrial metals, demand here is inelastic and tied to capital expenditure cycles of major tech firms. Verify exposure to these specific supply chains rather than general industrial health.

Precious metals like gold and silver often move inversely to real interest rates and the U.S. dollar. In 2026, if central banks maintain higher-for-longer rates, precious metals may underperform compared to industrial commodities. However, if inflation proves sticky, these assets serve as a hedge. Evaluate your portfolio’s correlation to the DXY (U.S. Dollar Index) to determine if you are overexposed to dollar strength.

Commodity prices are driven as much by supply shocks as by demand. Look for geopolitical risks in major mining jurisdictions or regulatory delays in new mine approvals. Supply chains for critical minerals are often concentrated in a few countries, making them vulnerable to trade policies. A shortage in one key region can spike prices globally, regardless of overall demand.

Low exchange inventories (LME, COMEX) signal tight markets and potential for price spikes. High inventories suggest oversupply and downward pressure. Track weekly inventory reports for copper and aluminum. These physical stock levels provide a real-time check on whether demand is outpacing the ability of mines to bring new production online.

Key Takeaways

- AI-driven data center growth creates structural demand for copper and aluminum.

- Precious metals act as a hedge against inflation and dollar weakness.

- Supply constraints and inventory levels are critical short-term price indicators.

- Diversify across industrial and precious metals to balance macroeconomic risks.

Common mistakes in 2026 commodity narratives

Investors often mistake structural shifts for temporary spikes. The 2026 commodity supercycle is not just about AI data centers; it is about the physical constraints of mining and refining. When analyzing metal prices, avoid these three misleading claims that could cost you capital.

Claim 1: "AI demand is a speculative bubble"

This view ignores the physical reality of power infrastructure. Data centers require massive amounts of copper for wiring and cooling. Goldman Sachs estimates data center power demand could double by 2030. This is not a bubble; it is a committed industrial load. Treating it as speculative ignores the multi-year lead times for copper mine development.

Claim 2: "Precious metals are only for hedging"

Morgan Stanley notes that gold and silver have a "bright outlook" beyond traditional safe-haven roles. Central banks are buying at record rates, while industrial demand for silver in solar panels and electronics grows. Viewing precious metals solely as a hedge against inflation misses their dual role as industrial inputs and monetary assets in a de-dollarizing trade environment.

Claim 3: "Base metals will crash if rates stay high"

This assumes demand is purely rate-sensitive. In 2026, base metal prices remain firm due to supply deficits, not just low rates. Mining capex has been underinvested for a decade. Even with higher borrowing costs, the physical shortage of refined copper and zinc supports prices. Relying on interest rate models alone fails to account for supply-side rigidity.

The market is pricing in physical scarcity, not just monetary policy. Check supply reports, not just Fed speeches.

2026 commodity trends: what to check next

Investors and industrial buyers are navigating a market where AI-driven demand intersects with traditional supply constraints. The following answers address the most common practical questions about the 2026 commodity supercycle, focusing on base metals, precious metals, and broader market shifts.

No comments yet. Be the first to share your thoughts!