Why the 2026 commodity supercycle is different

The current market cycle is structurally distinct from previous booms. It is not a simple cyclical recovery driven by temporary demand spikes or inventory restocking. Instead, the 2026 commodity supercycle is anchored by permanent structural shifts in global infrastructure and energy policy.

Two primary forces are reshaping the landscape. First, the rapid expansion of AI data centers has created a voracious, non-discretionary demand for copper, aluminum, and rare earth metals. Second, deglobalization and supply chain fragmentation have reduced the efficiency of global trade, forcing companies to hold higher inventory buffers and invest in redundant, often more expensive, domestic supply chains.

Years of underinvestment in new mines and processing facilities mean supply cannot respond immediately to these new demands. This mismatch between rigid supply and structurally rising demand creates a supportive backdrop for sustained commodity pricing, distinguishing this era from the volatile swings of the early 2000s or the post-2008 recovery.

How AI supply chains tighten copper and lithium markets

Artificial intelligence is no longer just a software story; it is a physical infrastructure build-out that is straining global commodity supplies. The expansion of data centers creates a direct, mechanical demand for copper and lithium, two metals that were already facing structural deficits before the AI boom accelerated.

The copper limits to account for

Every data center requires massive amounts of copper for electrical wiring, busbars, and cooling systems. A single hyperscale AI facility can consume hundreds of tons of copper, far exceeding the needs of traditional IT infrastructure. This demand is compounding with the electrification of vehicles and renewable energy grids, which also rely heavily on copper conductors.

Mining supply has struggled to keep pace. New copper projects face long lead times, permitting hurdles, and declining ore grades. The result is a tight market where demand growth outstrips the ability of miners to bring new capacity online quickly. This structural squeeze supports higher copper prices as data center operators compete for limited supply.

The Lithium Storage Gap

Lithium demand is driven by the need for energy storage and backup power systems. Data centers require robust battery backup to ensure uptime, and the broader grid needs storage to manage the intermittent nature of renewable energy sources. As AI workloads grow, so does the need for stable, reliable power, driving up lithium-ion battery production.

Battery manufacturing is scaling rapidly, but lithium mining and refining capacity are lagging. The extraction and processing of lithium are capital-intensive and environmentally regulated, slowing the pace of new supply. This mismatch between battery demand and lithium availability creates a bottleneck that keeps prices volatile and supply chains fragile.

Market Implications

The convergence of AI-driven demand and constrained supply is reshaping the commodity landscape. Investors and industry players are watching copper and lithium prices closely as indicators of broader economic trends. The AI supercycle is not just about chips and code; it is about the physical materials that power the digital world.

Technical charts for copper and lithium reflect this growing tension, showing upward trends as market participants price in future scarcity. The interplay between technological advancement and resource availability highlights the importance of supply chain resilience in the AI era.

| Metal | Primary AI Use | Supply Risk |

|---|---|---|

| Copper | Wiring & Cooling | High |

| Lithium | Battery Storage | Medium-High |

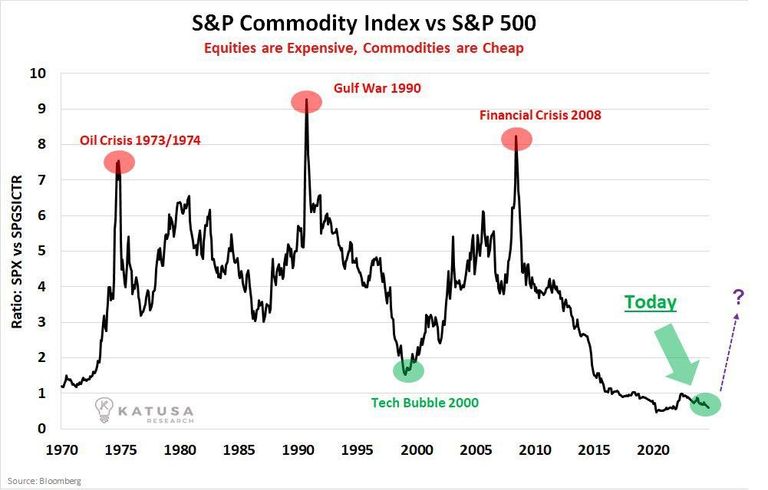

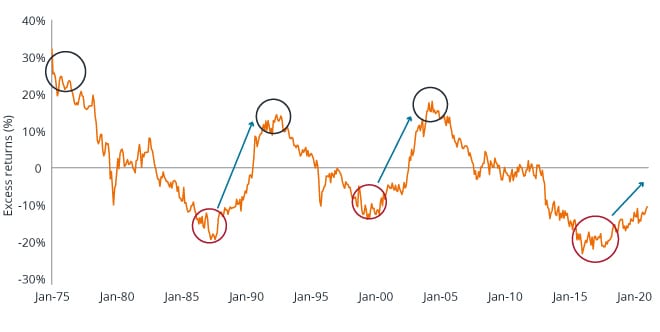

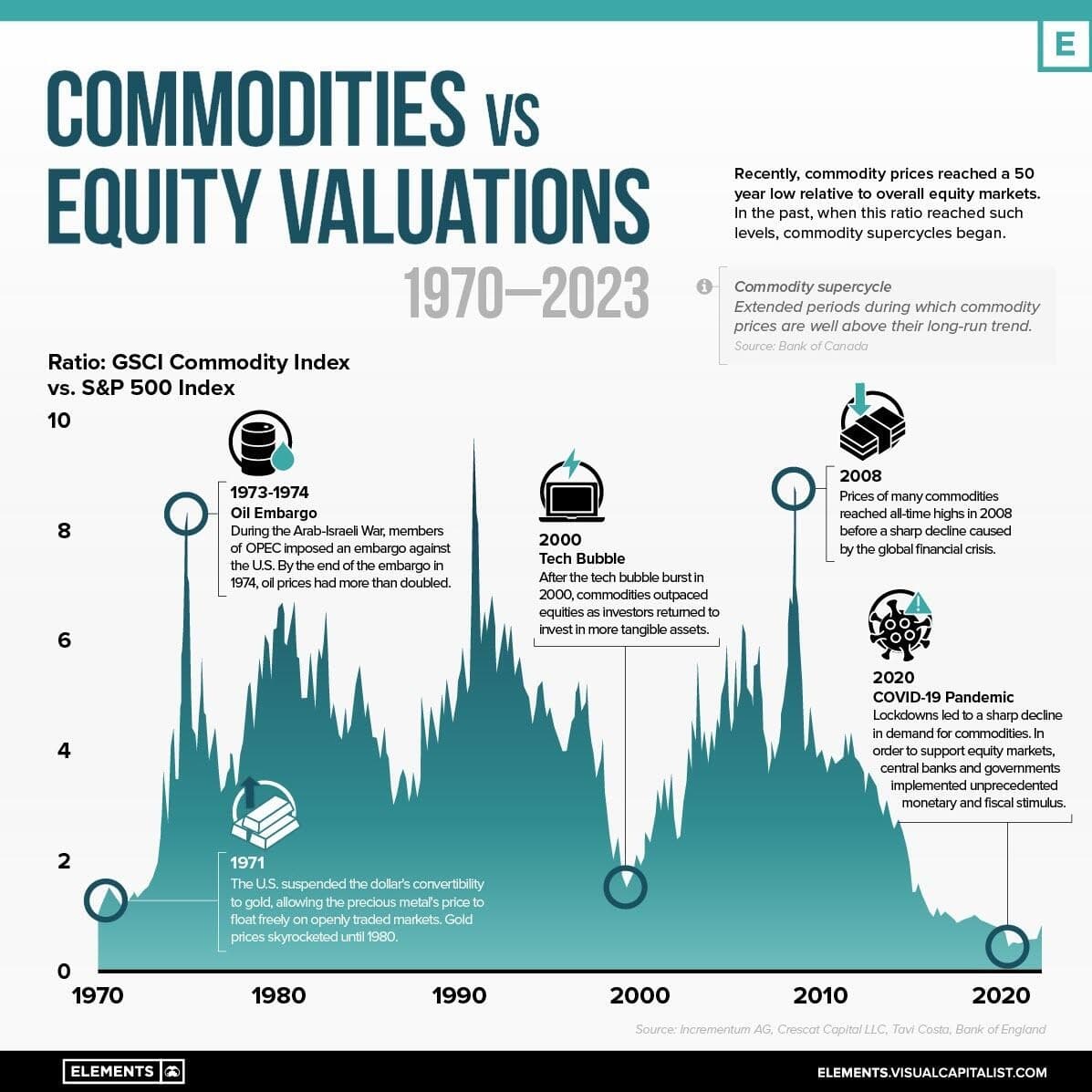

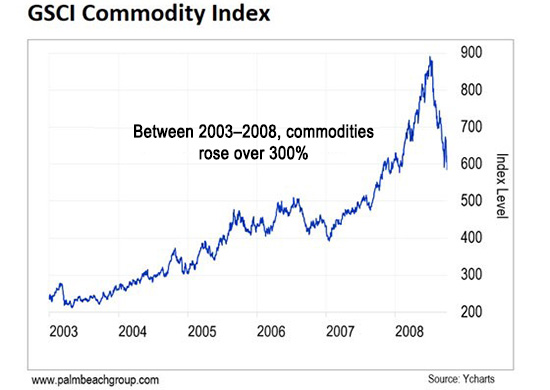

Copper price forecast 2026 and supply limits to account for

Copper is the primary indicator of the current commodity supercycle. Unlike speculative assets, copper demand is inelastic; it is required for electrification, grid expansion, and AI infrastructure. As the transition to green energy accelerates, the gap between mine supply and industrial demand is widening, creating a structural deficit that underpins price forecasts for 2026.

The supply side is constrained by aging assets and declining ore grades. Major producing regions, including Chile and Peru, are seeing the quality of extracted ore drop significantly. This means miners must process more rock to yield the same amount of copper, driving up operational costs and limiting the speed at which new supply can come online. These physical bottlenecks are not temporary; they represent a multi-year lag between capital investment and production.

Demand spikes from the AI sector and renewable energy projects are colliding with this tight supply. Data centers require massive amounts of copper for power distribution and cooling systems. Simultaneously, global decarbonization mandates are accelerating the replacement of fossil-fuel infrastructure with electric alternatives. This dual pressure creates a "small pool, big waves" scenario where even modest shifts in allocation or demand can trigger significant price volatility.

While some forecasts suggest broader commodity prices may face downward pressure due to oil gluts, copper remains distinct. Its role as a critical input for the digital and energy transitions ensures that supply constraints will likely keep prices elevated relative to historical averages, supporting a bullish outlook for the 2026 market cycle.

Lithium demand trends and battery storage growth

Lithium sits at the center of the energy transition, but its market behavior in 2026 reflects a complex tug-of-war between structural demand and short-term volatility. While the long-term trajectory for lithium carbonate remains upward due to electrification, the immediate landscape is defined by inventory adjustments and shifting battery chemistries. Understanding this dynamic requires looking beyond headline price spikes to the underlying mechanics of grid storage and electric vehicle production.

Grid-scale storage drives structural demand

The most significant shift in lithium demand is the move from transportation to stationary storage. As AI data centers and renewable energy grids require massive buffering capacity, lithium-ion batteries are becoming the default solution for frequency regulation and load balancing. This sector is less sensitive to short-term consumer trends and more driven by utility-scale infrastructure projects, creating a more stable demand floor. Energy storage requirements for AI grids are no longer a niche concern but a primary driver of industrial lithium consumption.

EV adoption faces temporary headwinds

Electric vehicle sales continue to grow, but the rate of acceleration has moderated in key markets. This slowdown has led to temporary oversupply in the lithium market, causing prices to dip from their 2022 peaks. However, this volatility is likely a correction rather than a structural decline. Manufacturers are adjusting production schedules to align with actual demand, reducing the risk of prolonged glut conditions. The focus is shifting toward cost efficiency and supply chain resilience rather than pure volume expansion.

Technical outlook and price signals

Tracking lithium prices requires attention to both spot market movements and long-term technical trends. The following chart illustrates the five-year trajectory of lithium carbonate, highlighting the extreme volatility that characterizes this market. Investors and industry participants should monitor these patterns to gauge future supply constraints and demand recovery.

Smart commodity trading strategies for 2026

Participating in the commodity supercycle requires more than just buying physical metals. The market is driven by structural shifts in AI infrastructure, decarbonization, and supply chain resilience. To capture gains while managing volatility, investors should use a layered approach that combines direct exposure with diversified financial instruments.

For most investors, broad commodity ETFs provide the safest entry point. These funds track baskets of metals like copper, gold, and lithium, smoothing out the volatility of individual assets. This approach ensures you capture the overall supercycle trend without betting on a single mine’s production output.

Once your base position is set, consider adding direct exposure to critical industrial metals. Copper and lithium are essential for AI data centers and electric vehicles. You can access these through futures contracts or physically backed ETFs. This step targets the specific supply constraints driving the current supercycle.

Traditional analysis often lags behind rapid market shifts. Use AI-driven trading platforms that analyze news, satellite imagery of mines, and shipping data in real time. These tools help identify supply disruptions before they appear in quarterly reports, allowing for quicker entry and exit points.

Don’t just invest in miners. Include companies involved in processing, refining, and recycling. These mid-stream and downstream players often benefit from higher volumes even if spot prices fluctuate. This diversification reduces risk if upstream mining projects face delays or regulatory hurdles.

Government policies on trade, tariffs, and green energy subsidies directly impact commodity prices. Stay updated on major economies’ infrastructure bills and export restrictions. Adjust your portfolio to align with these regulatory tailwinds, as they often dictate long-term demand more than short-term speculation.

By combining broad diversification with targeted AI insights and supply chain awareness, you can manage the complexities of the 2026 commodity supercycle. This strategy balances growth potential with risk mitigation, positioning you to benefit from the structural changes reshaping global markets.

No comments yet. Be the first to share your thoughts!