5 Raw Materials Driving Infrastructure

Global infrastructure projects are triggering a structural demand surge for specific raw materials, moving beyond abstract commodity indices to tangible assets. This section analyzes five critical inputs—copper, lithium, nickel, aluminum, and steel—backed by data from Janus Henderson and Carlyle, highlighting the physical metals and associated ETFs driving the 2026 supercycle.

-

Copper: The grid backbone for AI and EVs

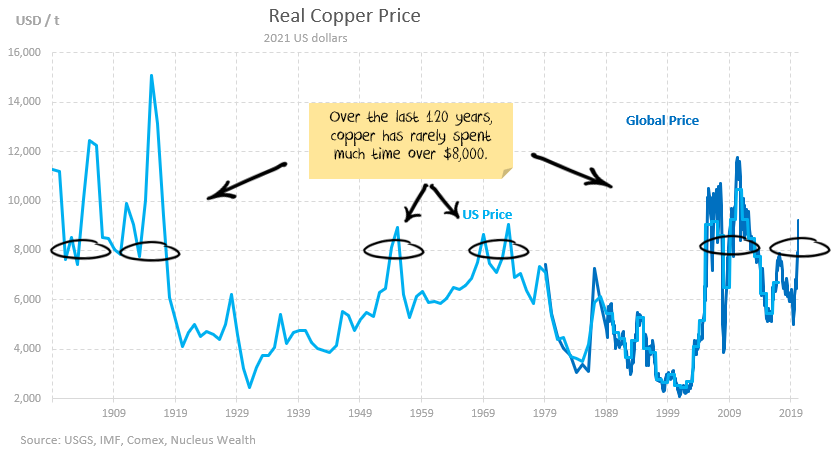

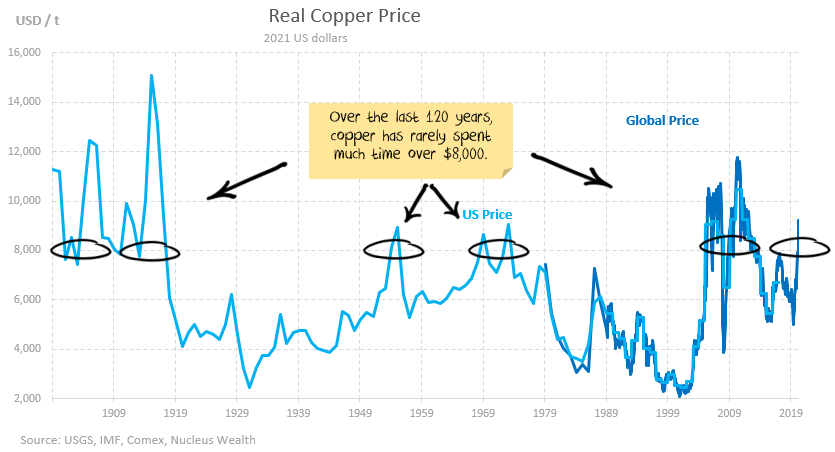

Copper remains the indispensable conductor for electrification, with data centers and electric vehicles demanding unprecedented volumes. Reuters reports that AI-driven power surges are tightening global supply, pushing prices toward record highs. Investors can access this exposure through physical holdings or ETFs like the Global X Copper Miners ETF (COPX). As infrastructure upgrades accelerate, copper’s role as the nervous system of modern grids ensures its premium status in the 2026 supercycle. -

Uranium: Powering the AI energy deficit

Artificial intelligence’s voracious energy appetite is driving a structural shift toward nuclear power, revitalizing uranium demand. The Oregon Group highlights that critical mineral investments must scale to meet these energy transition goals, with uranium acting as the baseload foundation. Physical uranium contracts and funds like the Sprott Physical Uranium Trust (SRUUF) offer direct exposure. As nations prioritize energy security, uranium’s scarcity and strategic value position it as a cornerstone of the clean energy infrastructure boom. -

Iron ore: Steel for global construction

Global infrastructure renewal requires massive quantities of steel, making iron ore the primary feedstock for construction projects worldwide. Carlyle notes that capital rotation into hard assets supports this demand, particularly in emerging markets rebuilding transport networks. Investors can track iron ore trends via ETFs like the Global X Steel ETF (SLX). Despite cyclical fluctuations, the long-term need for durable materials ensures iron ore remains a critical component of the commodity supercycle, underpinning urban expansion and industrial capacity. -

Aluminum: Lightweighting for transport

Aluminum’s low weight-to-strength ratio makes it essential for reducing emissions in automotive and aerospace sectors. Border States reports that March 2026 commodity updates highlight aluminum’s growing role in lightweighting strategies for electric vehicles and commercial transport. ETFs such as the iShares U.S. Aluminum ETF (AMZ) provide accessible exposure. As regulatory pressures mount for fuel efficiency, aluminum’s versatility in manufacturing ensures sustained demand, driving its importance in the broader infrastructure and transportation overhaul. -

Lithium: Battery storage for grid stability

Lithium-ion batteries are critical for storing renewable energy, ensuring grid stability as intermittent sources like solar and wind expand. Grand View Research projects significant market growth through 2033, driven by demand for energy storage systems. Investors can gain exposure through lithium-focused ETFs like the Global X Lithium & Battery Tech ETF (LIT). As utilities prioritize resilience, lithium’s role in balancing supply and demand cements its status as a vital raw material for the 2026 infrastructure supercycle.

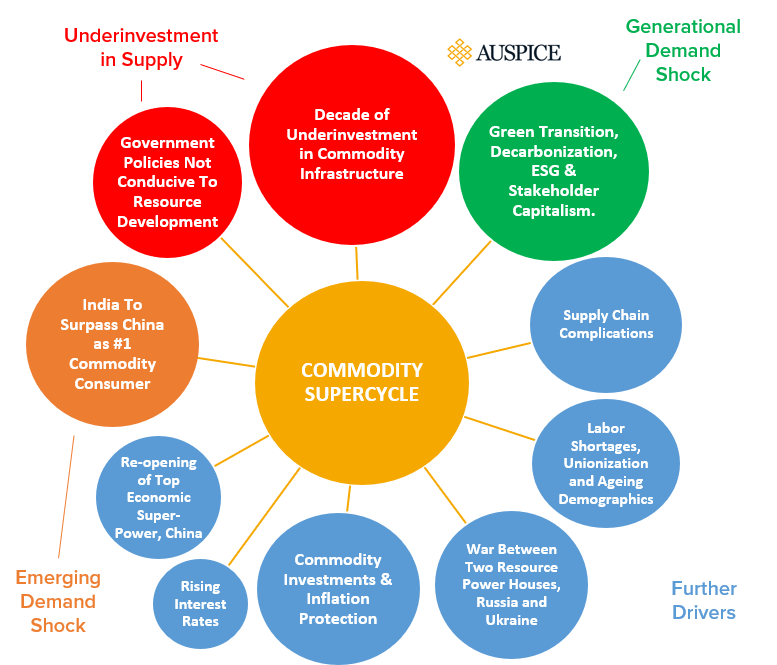

The 2026 commodity supercycle explained

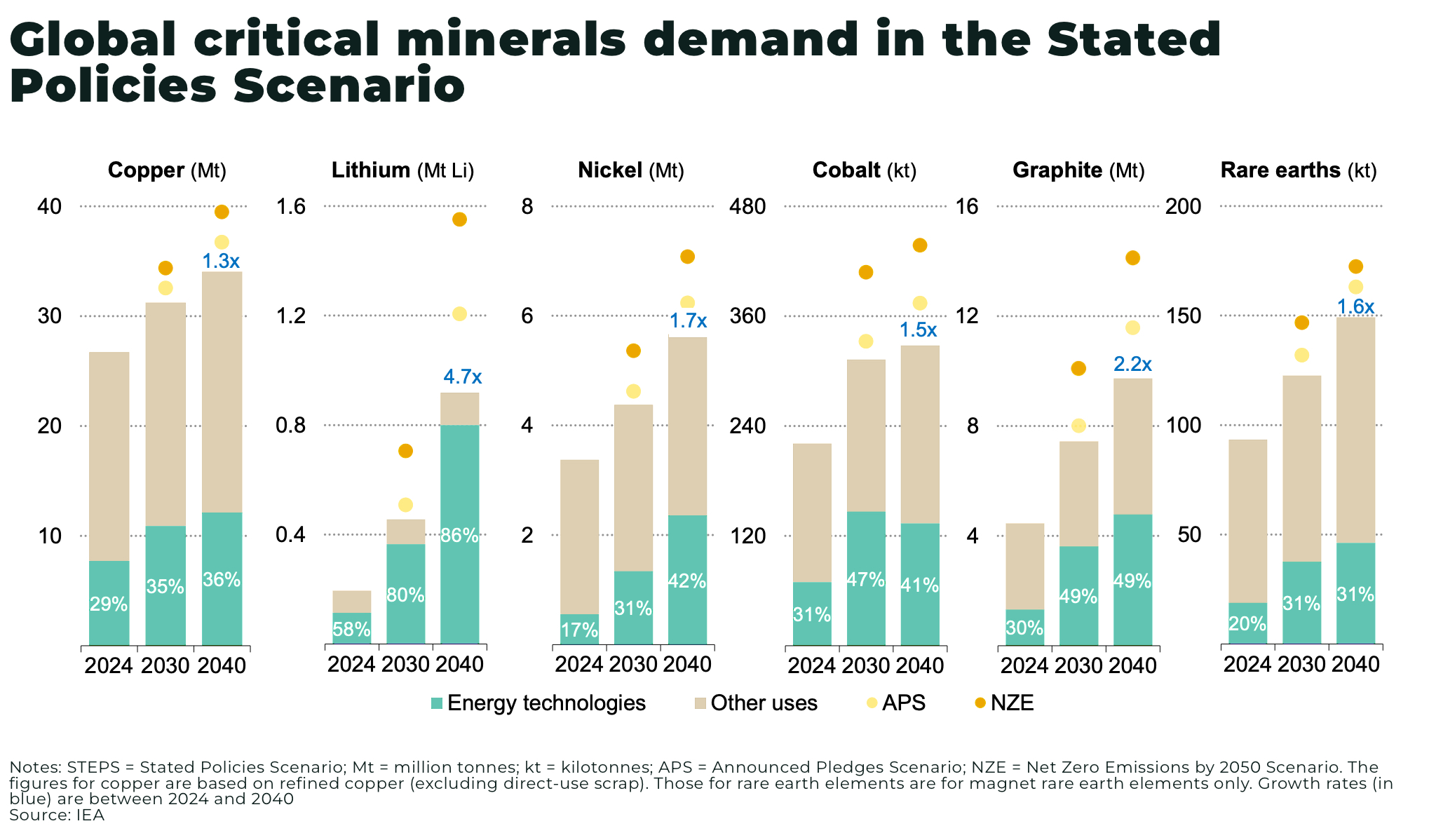

A commodity supercycle is defined as an extended period, typically lasting 20 to 30 years, where commodity prices remain well above their long-term historical averages due to structural demand outpacing supply [src-serp-2]. We are currently entering a phase analysts call "Supercycle 2.0," a distinct market cycle driven by three irreversible structural forces: deglobalization, decarbonization, and the infrastructure demands of artificial intelligence [src-serp-3].

Unlike previous cycles fueled primarily by emerging market industrialization, this cycle is anchored by the physical needs of the green transition and digital expansion. Decarbonization requires massive quantities of copper for electrical grids and aluminum for lightweighting, while AI data centers demand significant power infrastructure, further straining grid-capable materials [src-serp-3]. This convergence creates a supply deficit that traditional cyclical adjustments cannot quickly resolve.

The implications for investors are tangible. This environment favors exposure to specific raw materials rather than broad market indices. Physical commodities like copper and aluminum, alongside related financial instruments such as commodity-focused ETFs, serve as direct proxies for this infrastructure build-out. As supply chains restructure and green mandates accelerate, the premium for these critical materials is expected to persist, distinguishing this supercycle from shorter-term price spikes.

How to invest in the 2026 commodity cycle

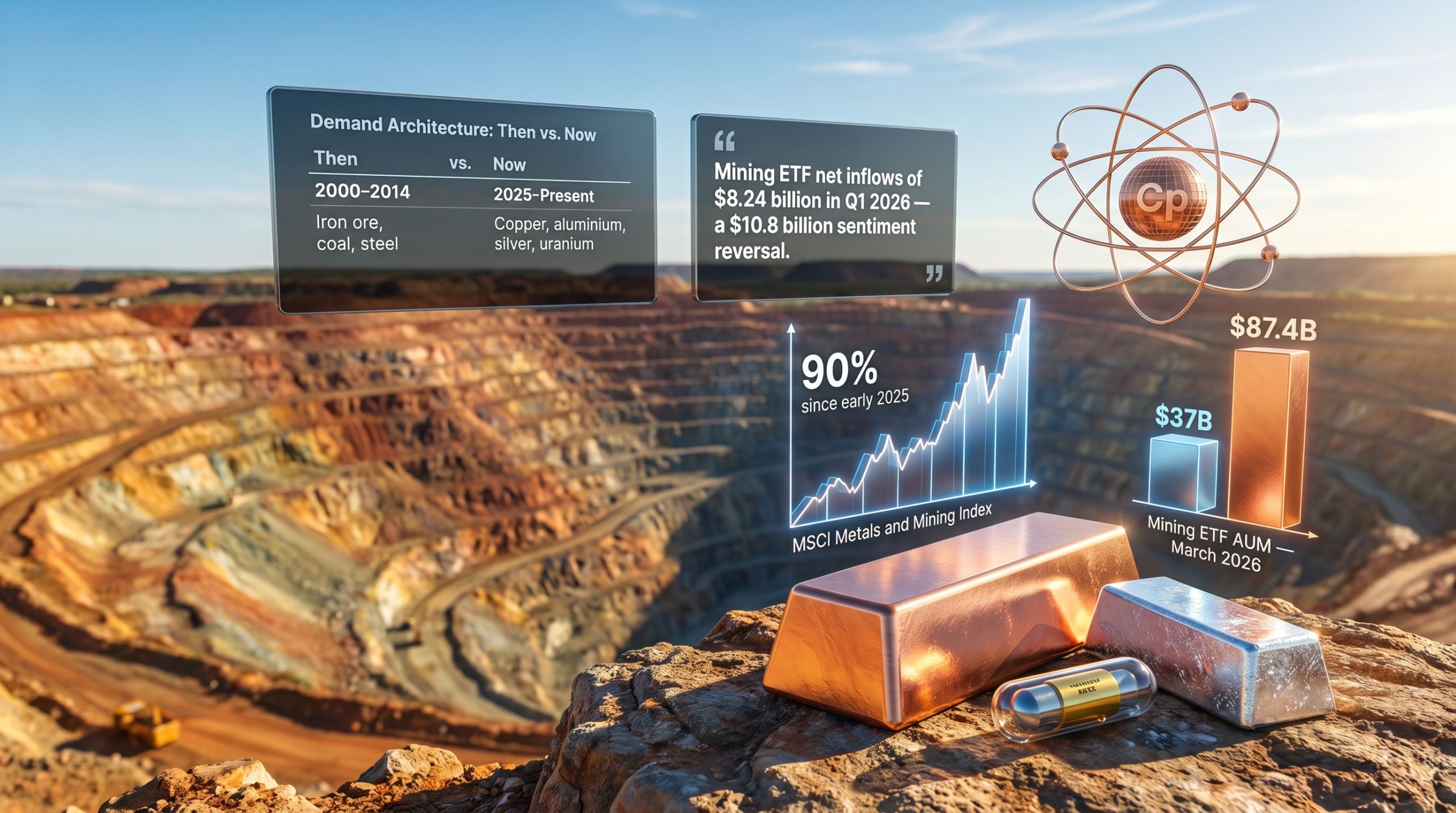

Participating in the 2026 commodity supercycle requires navigating a landscape defined by infrastructure demand and geopolitical volatility. The Iran war and global supply constraints have amplified price swings, making direct exposure to raw materials like copper, lithium, and iron ore both necessary and risky. Investors must choose instruments that balance liquidity with the structural reality that these materials are physical goods, not just financial derivatives.

Exchange-traded funds (ETFs) offer the most accessible entry point for institutional and retail investors alike. Products like the iShares S&P GSCI Commodity-Indexed Trust (GSG) or the Invesco DB Commodity Index Tracking Fund (DBC) provide diversified exposure to a basket of raw materials. This approach mitigates the risk of a single mine failure or supply disruption while capturing the broad upward trend driven by global infrastructure spending.

For those seeking higher conviction, targeted ETFs focusing on critical minerals offer direct exposure to the materials powering the energy transition. The Global X Copper Miners ETF (COPX) and the iShares MSCI Global Copper Miners ETF (COPX) allow investors to bet specifically on copper, the backbone of electrical grids and EVs. Similarly, lithium and cobalt-focused funds address the battery supply chain, though they carry higher volatility due to concentrated production in specific regions.

Physical ownership of metals like gold, silver, or copper bars provides a tangible hedge against currency devaluation and systemic financial risk. While storage and insurance costs apply, holding physical assets removes counterparty risk entirely. This strategy is best suited for long-term wealth preservation rather than short-term trading, as liquidity is lower and transaction spreads are wider than with paper contracts.

Choosing the right vehicle depends on your time horizon and risk tolerance. The table below contrasts the primary methods for participating in the cycle, highlighting the trade-offs between convenience, cost, and direct asset ownership.

| Vehicle | Direct Exposure | Volatility | Ongoing Cost |

|---|---|---|---|

| Commodity ETFs | Indirect (Futures/Stocks) | Moderate | Low (0.10-0.70% expense ratio) |

| Mining Stocks | Operational & Financial | High | Low (Brokerage commissions) |

| Physical Metals | Direct | Low (Price only) | High (Storage/Insurance/Spread) |

Commodities are historically more volatile than equities or bonds. A disciplined approach requires limiting any single commodity position to a small percentage of the total portfolio, typically 5-10%. This prevents a sudden spike in copper prices or a drop in iron ore demand from disproportionately impacting overall wealth. Regular rebalancing ensures that gains from one material do not lead to overexposure as prices rise.

For investors looking to hedge against inflation or secure physical assets, here are some popular options available for purchase:

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!