The 2026 commodity landscape

Global commodity markets are entering a period of fragmentation. While the World Bank forecasts that overall commodity prices will hit a six-year low by 2026, this aggregate decline masks a critical divergence in the supply chain. The era of uniform price drops is giving way to a landscape where general inputs soften, but essential materials remain under pressure.

Energy prices are falling, helping to ease global inflation, yet this relief is uneven. Industrial inputs face subdued demand, but the story changes drastically for the raw materials that power the modern economy. According to S&P Global’s Market Intelligence, while the general MPI for the second quarter of 2026 is forecast to be slightly below previous year levels, specific sectors are bucking the trend. This is not a blanket market correction; it is a structural shift where scarcity drives value.

The World Bank projects global commodity prices will drop to their lowest level in six years by 2026, marking the fourth consecutive year of decline.

Precious metals are emerging as a key counterpoint to this general deflation. Morgan Stanley highlights that gold and silver have a potentially bright outlook for 2026, driven by their dual role as financial hedges and industrial necessities. As supply chains restructure, the focus is no longer on volume alone, but on the resilience of specific materials.

5 Raw Materials Reshaping Supply Chains

As 2026 commodity trends accelerate, supply chains are pivoting toward five specific raw materials that are redefining industrial resilience. These shifts impact the physical components of everyday goods, from lithium-ion battery casings to aerospace-grade titanium alloys, rather than abstract market categories.

-

Lithium carbonate for EV battery production

Lithium carbonate remains the backbone of electric vehicle battery manufacturing, driving demand as automakers scale production. This raw material directly influences cathode chemistry and energy density. Supply chain resilience is critical, with major producers securing long-term contracts to meet the surging needs of the global EV market. 2026 commodity trends highlight this sector's volatility and strategic importance. -

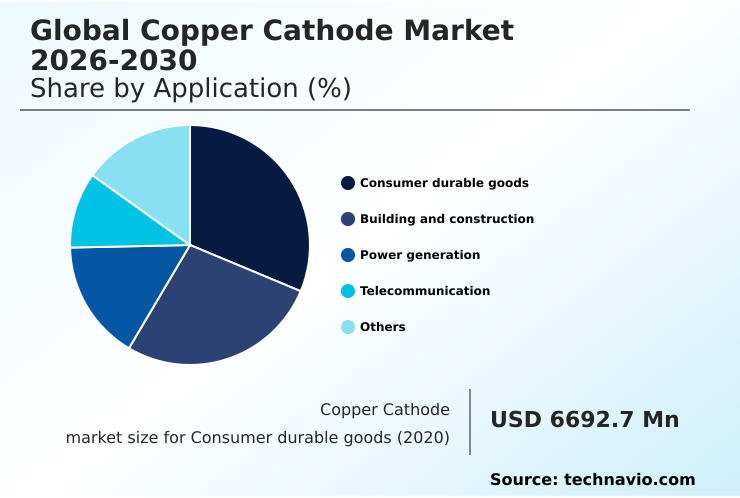

Copper cathode for electrical grid expansion

Copper cathode quality dictates the efficiency of new electrical grid infrastructure projects worldwide. As renewable energy integration accelerates, high-purity copper becomes essential for transmission lines and substations. Supply constraints are reshaping procurement strategies, forcing utilities to prioritize secure sourcing channels. This material is a cornerstone of the modernized power grid, reflecting key 2026 commodity trends. -

Nickel matte for stainless steel manufacturing

Nickel matte serves as a critical intermediate product for stainless steel manufacturing, supporting construction and industrial applications. Its purity levels directly impact the corrosion resistance and durability of final steel products. Fluctuating supply from major mining regions creates pricing pressure, making inventory management vital for manufacturers navigating these 2026 commodity trends. -

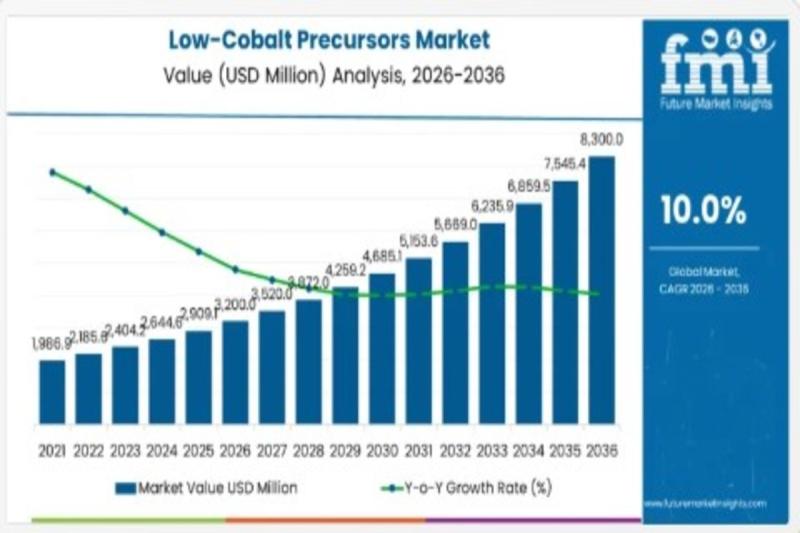

Cobalt hydroxide for energy storage systems

Cobalt hydroxide is a primary precursor for lithium-ion batteries used in stationary energy storage systems. Its role ensures stable voltage output and longer cycle life for grid-scale storage solutions. Ethical sourcing and supply chain transparency are becoming major factors as demand grows. This material's trajectory is central to understanding current 2026 commodity trends. -

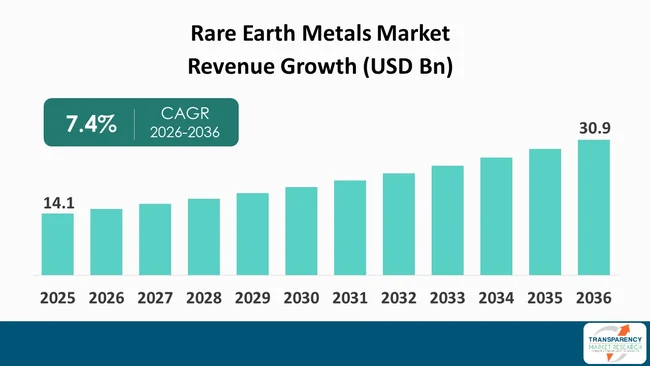

Rare earth oxides for permanent magnets

Rare earth oxides are indispensable for producing high-performance permanent magnets in wind turbines and electric motors. Neodymium and praseodymium oxides specifically enable the strong magnetic fields required for efficient energy conversion. Geopolitical supply concentrations create significant risk, prompting diversification efforts. This sector's dynamics are a defining feature of 2026 commodity trends.

Critical minerals for energy transition

The 2026 commodity trends landscape is defined by the race for critical minerals. Lithium, cobalt, and rare earth elements are no longer niche materials; they are the foundational inputs for the global energy transition. As supply chains restructure, these minerals dictate the pace of electric vehicle adoption and renewable energy deployment.

Lithium and cobalt: The battery backbone

Lithium and cobalt remain the primary drivers of energy storage demand. Lithium carbonate prices have stabilized as extraction capacity in Australia and South America meets growing battery production needs. Cobalt supply remains tighter, with the Democratic Republic of Congo still controlling the majority of global output. This concentration creates supply chain vulnerabilities that manufacturers are actively trying to mitigate through recycling and alternative chemistries.

Rare earths: The magnets that drive efficiency

Rare earth elements, particularly neodymium and praseodymium, are essential for high-performance permanent magnets used in wind turbines and EV motors. China currently dominates the refining capacity for these materials, making supply security a top priority for Western industrial policy. Diversifying sourcing to projects in Australia and the United States is a key focus for 2026 supply chain strategies, aiming to reduce geopolitical risk.

Supply chain resilience strategies

Companies are moving beyond simple procurement to secure long-term offtake agreements. The USGS Mineral Commodity Summaries 2026 highlights how policy shifts and tariffs are reshaping trade flows. Investors and industrial buyers alike are focusing on vertical integration, securing direct access to mine sites and processing facilities to ensure stable 2026 commodity trends amid global uncertainty.

Base metals and infrastructure demand

Infrastructure spending and construction recovery are the primary drivers supporting base metal prices in 2026. While energy and precious metals react to geopolitical shifts and inflation hedging, base metals like copper, aluminum, and zinc are tied directly to physical building activity. The World Bank’s latest outlook notes that global commodity prices are expected to drop to their lowest level in six years by 2026, yet infrastructure demand provides a distinct floor for these specific materials [1].

This demand is not abstract. It is visible in the procurement of raw materials for grid modernization, housing starts, and public works. Copper remains essential for electrical wiring and renewable energy connections, while aluminum and zinc are critical for structural framing and corrosion protection. Fastmarkets highlights that analyzing supply and demand trends for these metals is central to understanding the 2026 commodity trends [2].

The distinction between industrial inputs and infrastructure support is clear. Industrial inputs often fluctuate with consumer electronics cycles or automotive production shifts. Infrastructure demand, however, is driven by long-term capital projects with multi-year timelines. This stability helps decouple base metal prices from the more volatile swings seen in other sectors.

[1] World Bank Group. "Global Commodity Price Outlook." [2] Fastmarkets. "2026 commodity market outlooks."

Gold and Silver as Safe Havens

Precious metals remain a cornerstone of the 2026 commodity trends outlook, acting as a defensive buffer against market volatility. As central banks navigate shifting interest rate policies and inflation concerns linger, investors are increasingly turning to gold and silver to preserve capital. Morgan Stanley highlights that beyond fuels and industrial inputs, precious metals offer a potentially bright outlook for the year, driven by their role as a hedge against currency debasement and geopolitical uncertainty.

Gold serves as the primary anchor in this strategy. Its value is less about immediate yield and more about stability during turbulent periods. When equity markets face headwinds or when the U.S. dollar shows signs of weakness, gold typically absorbs the shock, providing a counterbalance to riskier assets. This dynamic makes it an essential component for portfolios seeking to mitigate downside risk in the current economic landscape.

Silver complements this safety net with a dual identity. While it shares gold’s monetary heritage, silver also has significant industrial applications in solar panels, electronics, and electric vehicles. This industrial demand adds a layer of complexity to its price action; it can outperform gold during economic recoveries but may lag during industrial slowdowns. For investors, this means silver offers growth potential alongside its safe-haven credentials, though with higher volatility.

The interplay between these metals and the broader macro environment is critical. A weakening U.S. dollar often boosts precious metals prices, as they become cheaper for holders of other currencies. Conversely, rising real interest rates can pressure prices, as non-yielding assets become less attractive. Understanding these drivers is key to positioning within the 2026 commodity trends framework.

Energy markets and LNG growth

The 2026 commodity trends are defined by a structural shift in how energy moves across borders. While oil markets stabilize after years of volatility, liquefied natural gas (LNG) has become the primary driver of global trade route adjustments. Energy trading houses are pivoting capital toward transition metals and LNG infrastructure, reflecting a broader industry move away from pure fossil fuel speculation toward diversified energy trading.

LNG capacity expansions in the United States and Qatar are redirecting flows from traditional Asian contracts to European and emerging markets. This diversification reduces reliance on single-source pipelines and creates new arbitrage opportunities. As noted by industry analysts, the shift is not merely cyclical but structural, with trading firms embedding data-driven logistics into their core strategies to manage these new routes.

Oil prices remain constrained by steady non-OPEC production growth, particularly from the United States and Brazil. This abundance prevents the supply shocks that characterized previous years, keeping inflationary pressures in check. The World Bank’s latest Commodity Markets Outlook confirms that energy prices are contributing to a broader easing of global inflation, with 2026 projected to see prices at their lowest level in six years.

The convergence of stable oil and growing LNG trade creates a complex but predictable landscape for 2026. Investors and traders are focusing on infrastructure bottlenecks and regulatory changes rather than raw supply deficits. This maturation of the energy market means that 2026 commodity trends will be less about scarcity and more about the efficiency of distribution and the speed of adaptation to new global trade patterns.

Navigating 2026 commodity risks

The 2026 commodity landscape is defined by fragmentation. Energy trading houses are pivoting toward transition metals, while oil majors shift focus to LNG. This diversification creates a complex web of interdependencies where a disruption in one sector ripples through others. To manage these risks, traders must move beyond intuition and adopt data-driven strategies that account for these structural shifts.

Diversification is no longer just a buzzword; it is a survival mechanism. Relying on a single commodity or region exposes portfolios to volatile geopolitical and climate shocks. Instead, successful firms are building resilience through multi-asset exposure and real-time analytics. They are using advanced data models to predict price fluctuations caused by energy transitions and supply chain bottlenecks. This approach allows them to hedge effectively against the unpredictable nature of the current market.

For those looking to deepen their understanding of these dynamics, several essential resources provide the frameworks needed to navigate this volatility. These books offer concrete strategies for managing risk in a fragmented market, helping traders and analysts stay ahead of the curve.

As an Amazon Associate, we may earn from qualifying purchases.

Frequently asked questions on 2026 commodity trends

Can commodity prices hit new lows in 2026?

Yes. According to the World Bank’s latest Commodity Markets Outlook, global commodity prices are projected to drop to their lowest level in six years by 2026. This marks the fourth consecutive year of decline, driven largely by falling energy prices that are helping to ease global inflation pressures.

Will 2026 commodity trends stabilize supply chains?

Stability is unlikely in the near term. S&P Global’s March 2026 report notes that while prices are returning to year-earlier levels, the MPI for the second quarter of 2026 is forecast to be 0.4% below the previous year. Markets are entering a more fragmented phase, requiring supply chain managers to adapt to continued volatility rather than expecting immediate normalization.

How do 2026 commodity trends affect raw material costs?

For manufacturers, the downward trend means lower input costs for raw materials, but not necessarily lower final prices. BrainWorks’ 2026 Commodity Market Outlook highlights that subdued global demand is the primary driver of these price declines. Companies may see improved margins if they can lock in purchases before further dips, but the overall market sentiment remains cautious.

No comments yet. Be the first to share your thoughts!