The Macro Backdrop for 2026

The macroeconomic environment in 2026 is setting the stage for a distinct rotation within commodity markets. While energy and fertilizer prices have surged, the broader narrative is being shaped by a convergence of monetary policy shifts and resilient global growth. This backdrop creates a favorable terrain for critical minerals, which are increasingly decoupling from general industrial demand to serve specific energy transition needs.

Global economic expansion remains sturdy, defying earlier recession fears. According to Goldman Sachs, the base case for 2026 includes continued global GDP growth alongside a projected 50 basis points of Federal Reserve rate cuts. This monetary easing is historically supportive of top-down commodity returns, as lower borrowing costs reduce the carrying cost of holding physical assets and stimulate capital-intensive industrial projects.

Simultaneously, the US dollar is showing signs of weakness, a key tailwind for dollar-denominated commodities. A softer greenback makes raw materials cheaper for holders of other currencies, boosting demand. The chart below illustrates the recent trajectory of the US Dollar Index (DXY), highlighting the inverse relationship that often exists between dollar strength and commodity price rallies.

Despite these supportive macro factors, price moderation persists in certain sectors. The World Bank projects that overall global commodity prices will decline by approximately 7 percent in 2026, marking the fourth consecutive year of moderation. This divergence underscores why the rally is not uniform; while energy and critical minerals benefit from structural supply constraints and policy mandates, other commodities face headwinds from slowing demand in major economies.

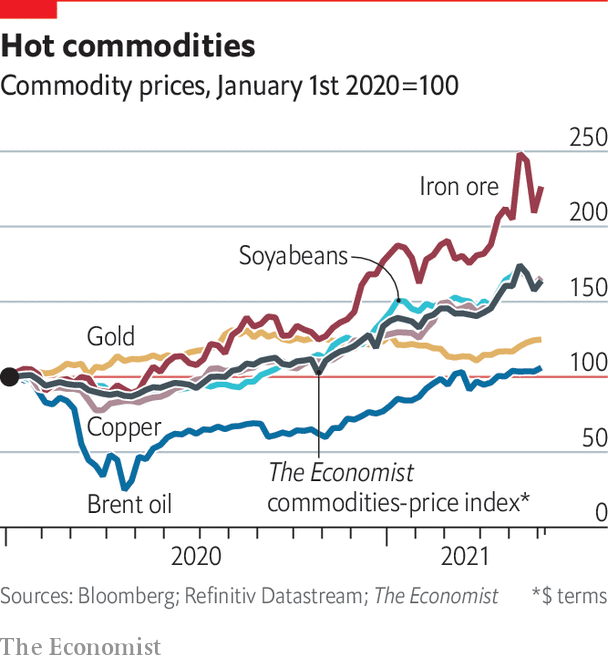

Critical minerals lead the rally

The 2026 commodity landscape is defined by a sharp divergence between traditional energy assets and the materials powering the green transition. While oil prices fluctuate with geopolitical noise and gold serves as a defensive hedge, critical minerals like lithium, copper, and nickel are experiencing structural outperformance. According to the World Bank’s April 2026 Commodity Markets Outlook, overall commodity prices are forecast to rise 16%, driven largely by record-high prices for these key metals alongside soaring energy and fertilizer costs [1].

This rally is not merely cyclical; it is structural. The supply side faces a chronic deficit, as new mining projects take a decade or more to come online, while demand from electric vehicle (EV) manufacturing and renewable energy infrastructure accelerates. Goldman Sachs and other major financial institutions highlight that this supply-demand imbalance creates a sustained upward pressure on prices, distinguishing these assets from the more volatile fossil fuel markets.

Copper, often called "dr. Copper" for its sensitivity to economic health, is central to this trend. Its conductivity makes it indispensable for grid modernization and EVs, yet global reserves are being depleted faster than new discoveries can replace them. Similarly, lithium and nickel, the backbone of battery technology, are seeing demand outstrip mining capacity. This creates a high-stakes environment where access to these minerals is becoming a strategic priority for governments and corporations alike.

The contrast with gold and silver is notable. While precious metals remain strong and act as leadership areas during periods of US dollar weakness, their role is primarily financial or inflationary [3]. Critical minerals, by contrast, are driven by physical industrial necessity. Their price trajectories are tied to tangible adoption rates of green technology, making them a distinct asset class with different risk and reward profiles. Investors are increasingly recognizing that the transition to a low-carbon economy is a material-intensive process, not just a policy one.

Energy trading houses pivot to transition metals

Energy trading houses are moving aggressively into transition metals, while traditional oil majors are pivoting toward liquefied natural gas (LNG). This divergence creates new investment dynamics as the industry balances decarbonization mandates with near-term energy security needs.

According to the World Bank’s April 2026 Commodity Markets Outlook, overall commodity prices are forecast to rise 16% this year. This surge is driven by soaring energy and fertilizer costs, alongside record-high prices for key metals. The data underscores that the energy transition is not just a long-term trend but an immediate price driver.

To understand the shift, compare the exposure of traditional energy indices against those focused on transition metals. The table below highlights the difference in volatility and growth potential between these two sectors.

| Metric | Traditional Energy | Transition Metals | LNG Sector |

|---|---|---|---|

| Primary Driver | Oil demand | EV & Grid buildout | Europe & Asia demand |

| Volatility Profile | High | Very High | Moderate |

| 2026 Price Forecast | Flat to +5% | +15-20% | +10-12% |

| Key Risk | Demand destruction | Supply bottlenecks | Infrastructure delays |

Goldman Sachs notes that this pivot is reshaping portfolio strategies. Investors are no longer choosing between fossil fuels and green energy; they are navigating a hybrid market where LNG acts as the bridge and transition metals provide the growth engine. Understanding these distinct risk profiles is essential for capitalizing on the 2026 commodity rally.

2026 Price Forecasts and Risks

The 2026 commodity landscape is defined by a sharp divergence between broad moderation and specific metal strength. While the World Bank’s April 2026 Commodity Markets Outlook projects a 16% rise in overall commodity prices, this aggregate figure is driven primarily by soaring energy, fertilizer, and key metal costs. This upward pressure contrasts with the broader trend of a 7% decline in non-energy, non-metals prices, marking the fourth consecutive year of general moderation. The market is not rising uniformly; it is being pulled higher by a concentrated rally in critical minerals and energy inputs.

Goldman Sachs and other institutional analysts point to structural supply deficits in copper and lithium as the primary drivers for the metals segment. Unlike the volatile agricultural or energy sectors, which face demand-side uncertainty, the critical minerals market is constrained by long lead times for new mine development. This supply rigidity means that even modest demand growth from the green energy transition can trigger significant price spikes. Investors are pricing in these constraints, leading to a risk premium that extends beyond simple supply-demand mechanics.

Critical Minerals: The Growth Engine

Critical minerals are the standout performers in the 2026 forecast. Copper prices are projected to remain elevated as utility-scale renewable projects and grid modernization efforts accelerate globally. Lithium, after a brutal correction in 2024 and 2025, is expected to stabilize at higher levels as battery production scales and older, high-cost mines shut down. These metals are not just commodities; they are strategic assets with limited substitutability. Their price trajectories are decoupling from traditional industrial cycles, reflecting their new role as foundational inputs for the energy transition.

Risks and Downside Scenarios

Despite the bullish outlook for metals, significant risks remain. A deeper-than-expected global economic slowdown, particularly in China, could dampen demand for industrial metals. Additionally, geopolitical tensions affecting supply chains for rare earth elements or cobalt could introduce sudden volatility. The World Bank notes that while energy prices are expected to moderate from their peaks, they remain susceptible to supply shocks. Traders must monitor these macro indicators closely, as the 16% overall price rise masks the potential for sharp corrections in specific sub-sectors.

| Commodity | 2026 Forecast | Primary Driver |

|---|---|---|

| Copper | Bullish | Supply deficit, energy transition |

| Lithium | Stabilizing | Battery demand, mine closures |

| Crude Oil | Moderate | OPEC+ policy, global demand |

| Agriculture | Declining | Improved harvests, lower demand |

Frequently asked: what to check next

What will the commodity index be in 2026?

The World Bank forecasts that overall commodity prices will rise by 16% in 2026. This rebound is driven by soaring energy and fertilizer prices, alongside record-high valuations for several key metals. The next update to this outlook is scheduled for October 2026.

Which commodities are leading the rally?

Energy and fertilizer markets are primary drivers of the projected price increase. Additionally, several key metals are trading at record-high levels. These sectors are contributing most significantly to the overall 16% rise in the commodity index.

What are the downside risks for commodity investors?

A deeper-than-expected global economic slowdown, particularly in China, could dampen demand for industrial metals. Additionally, geopolitical tensions affecting supply chains for rare earth elements or cobalt could introduce sudden volatility. The World Bank notes that while energy prices are expected to moderate from their peaks, they remain susceptible to supply shocks.

No comments yet. Be the first to share your thoughts!